Uncover the operational intricacies of this commonplace technology and understand the significance of selecting appropriate hardware.

You’ve tapped, you’ve swiped, you’ve experienced approvals and declines. Your engagements with EFTPOS have been numerous, yet the inner workings of this ubiquitous technology may remain unknown. While many can blissfully navigate cashless transactions, business owners must understand the intricacies of EFTPOS transactions, their functioning, and the selection of appropriate hardware. Continue reading for a comprehensive breakdown of everything you need to know about EFTPOS, along with practical guidance for choosing the right terminal.

What is EFTPOS?

EFTPOS, short for Electronic Funds Transfer at Point Of Sale, is an electronic payment system enabling customers to transfer funds from their bank account to a merchant’s business account during transactions. In simpler terms, it refers to any device accepting debit and credit card payments. In the contemporary business landscape, possessing an EFTPOS terminal proves advantageous. It provides a convenient and efficient means of accepting digital transfers, offering quick payment processing, automated record-keeping, and a reduction in cash handling.

The Rise of EFTPOS

Introduced to the Australian market in 1984, the EFTPOS transaction system faced a gradual acceptance period as both business owners and consumers adapted to the concept of digital payments. To provide context, as of 1985, Australians predominantly used cash for 90% of all transactions. It wasn’t until 2002 that the EFTPOS industry experienced significant growth. During this period, EFTPOS terminals were exclusively manufactured by the four major Australian banks and featured functional yet unwieldy designs.

In the contemporary landscape, there have been notable changes on both sides of the transaction. Customers have increasingly embraced electronic payments, with widespread adoption of debit and credit cards and, more recently, mobile wallets. For merchants, there has been a remarkable evolution in EFTPOS hardware. Modern terminals not only come in a variety of sleek styles to complement the aesthetic of businesses but also offer enhanced functionality to manage finances and elevate the customer experience. This includes features such as surcharging, tipping options, and Pay at Table technology.

The momentum toward a cashless society, already in progress, received a significant boost from the COVID-19 pandemic. Since early 2020, business owners and customers across Australia have rapidly sought to minimize cash handling due to health concerns associated with physical money exchange. In 2021, the Reserve Bank of Australia reported that only 27% of in-person payments were made using cash.

EFTPOS VS. eftpos

Adding to the complexity, “eftpos” (in lowercase) also designates a privately-operated Australian debit card platform. While “EFTPOS” serves as the globally recognized term denoting the link between a customer’s bank account and a business bank account (or Zeller Transaction Account), “eftpos” is the brand name for a specific payment system. The crucial distinction with “eftpos” lies in its exclusive support for debit cards—excluding credit cards—and its operation limited to Australia.

It’s probable that you may not have noticed this subtle divergence, primarily because 90% of all debit cards in Australia are co-branded with Visa or Mastercard. This co-branding allows these cards to process transactions through Australia’s local debit card network, known as “eftpos,” as well as international schemes. When a customer taps, dips, or swipes their “eftpos” card and chooses either Cheque or Savings, the transaction is routed through the “eftpos” network. However, if the customer opts for a Credit payment, the transaction is processed through Visa or Mastercard, as credit payments cannot be facilitated through “eftpos.” While delving into the specifics might be intricate, it’s essential to recognize the disparity between “EFTPOS” and “eftpos” when seeking a card-processing terminal.

How do EFTPOS transactions work?

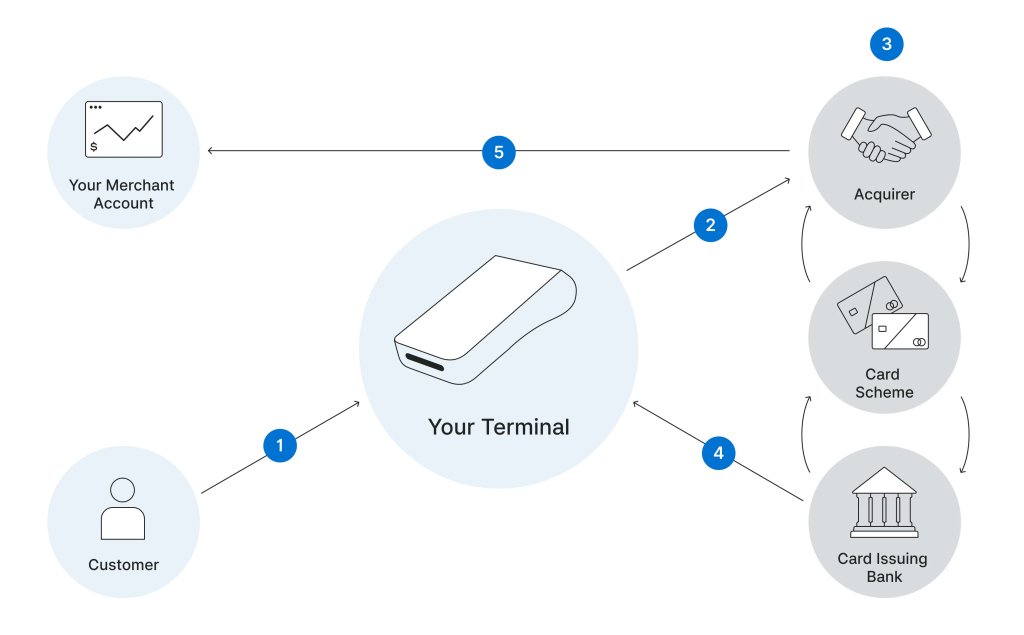

EFTPOS transactions initiate with the use of an EFTPOS machine, serving as the conduit through which various networks interconnect and exchange information to facilitate a seamless payment process. The involved networks encompass the buyer’s bank, the merchant’s business bank account, the EFTPOS machine provider, and, more recently, the point-of-sale (POS) technology. The communication between the terminal on the counter and these broader networks ensures that the utilized card possesses adequate funds in its associated account, verifies the cardholder’s identity, and confirms the bank linked to the card. In cases where the machine integrates with your POS software, it collaborates with the system to display the relevant transaction amount on the terminal. The provided image delineates the sequential operation of this system.

The Acquirer, such as Zeller, denotes the financial institution responsible for processing the payment on behalf of the merchant.

The Card Scheme, also referred to as a payment network or payment scheme, is the entity that establishes and maintains the rules and infrastructure governing the use of credit and debit cards. Examples include Visa, Mastercard, and American Express.

The Card Issuing Bank is the financial institution supplying a credit or debit card to the customer.

How long do EFTPOS transactions take?

Despite the instantaneous nature of the transaction, the multi-step process involving authentication, verification, and funds transfer, as outlined above, may require some time for complete processing. The speed at which your money “settles,” i.e., becomes available in your bank account, varies among different EFTPOS terminal providers. This aspect holds significant importance when selecting your payments platform, as the time it takes to access your funds can significantly impact your business cash flow. For instance, Zeller customers settling to their Zeller Transaction Account can expect to receive their funds on a nightly basis, whereas other platforms may take up to 72 hours.

What to look for in an EFTPOS machine

When selecting an EFTPOS terminal for your business, it’s crucial to ask nine key questions. While evaluating initial expenses like terminal and setup fees, as well as considering functionality and mobility, ensure your chosen terminal also satisfies the following criteria to maximize its value:

When choosing an EFTPOS terminal for your business, ensure it meets the following criteria:

- Accepts All Card Types:

As a business owner in Australia, it’s essential that your terminal can process eftpos debit cards along with widely used international standards such as Visa, Mastercard, and American Express. - Accepts Contactless Payments:

With the increasing popularity of NFC technology, ensure your terminal supports contactless payments, facilitating quick and convenient transactions through “tap-and-go” methods with both cards and mobile wallets. - Low and Flat Merchant Fees:

Look for a terminal with low and flat EFTPOS transaction fees, providing predictability in processing costs. At Zeller, for example, the flat fee is 1.4% per transaction, regardless of the chosen payment method. - Option for Surcharging:

Opt for a terminal that offers the option of surcharging, also known as zero-cost EFTPOS. This feature allows you to pass on transaction fees to the customer, serving as a cost-cutting measure for your business. - Multiple Connectivity Options:

Choose a terminal that provides multiple connectivity options. In case of WiFi disruptions, having a SIM card in the EFTPOS machine ensures seamless payment processing even when the primary connection is down. This redundancy guarantees uninterrupted business operations.